2021 Has Arrived, But What Does That Really Mean?

For most of us 2020 couldn’t end soon enough. (If you’re one of them, check out John Oliver’s end of year stunt. It’s immensely satisfying).

Now, after months of looking longingly to 2021, the moment has finally arrived. But what does the New Year really mean for our lives and our business? Here are some key questions we’re tracking as 2021 unfolds.

Is the e-commerce boom here to stay?

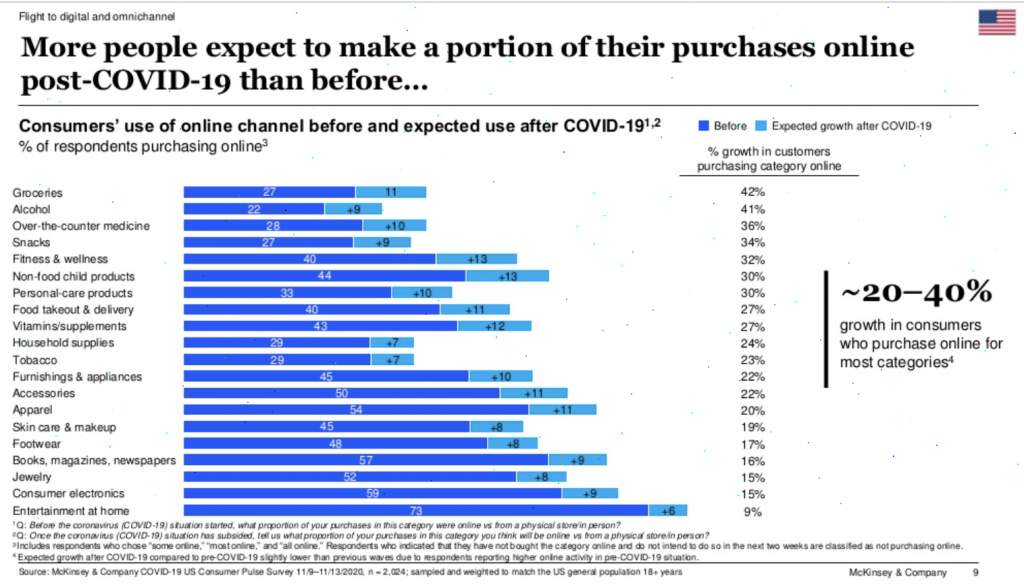

2020 was a bad year for brick-and-mortar retail, yes, but it was a banner one for e-commerce with major retailers like Target, Tesco, Walmart, Carrefour and others reporting huge bumps (like more than 100% huge, in some cases) in their online business.

A lot of this was a factor of circumstance. In many cases, consumers around the world had no other choice but to buy online. So now, as business begins to return to normal, the question on everyone’s mind is what shoppers will do once they have a choice again.

The general consensus appears to be that the e-commerce boost is here to stay, with 3 out of 4 Americans reporting that they tried a new shopping behavior during the pandemic and most of them signaling they intend to continue even when the crisis is past.

Now, just to put things in context, ecommerce still accounts for a relatively small portion of total retail revenue. Worldwide, ecommerce’s share of the retail sales pie averaged around 17.3% in 2020, but that is still a huge jump from where things stood in 2019.

And the fact is, people will return to stores. But brick-and-mortar retailers are going to have to sell the in-store experience like they never have before, and the bar has been raised when it comes to consumer expectations. A flawless e-commerce experience is now a baseline requirement for any major retailer and, as store visits become the norm again, we expect demand for seamless omnichannel shopping experiences to increase as well.

What will be the state of film and entertainment distribution once theaters reopen?

“Wonder Woman: 1984” was the first feature in Warner Bros’ slate to release simultaneously on streaming and in theaters on Christmas Day, setting the precedent for the studio’s 17 releases this year.

“Wonder Woman: 1984” was the first feature in Warner Bros’ slate to release simultaneously on streaming and in theaters on Christmas Day, setting the precedent for the studio’s 17 releases this year.

Last month Warner Bros. and Disney both announced that they would release large chunks of their content slate for streaming and in theater simultaneously.

Warner will use this strategy for all 17 of its feature films this year. Meanwhile, of the 100 films and TV series Disney announced at its investor day in December, 80% are going to Disney Plus first.

Clearly this is the strategy for 2021. What’s less clear is whether this is simply a stop-gap measure to get through the pandemic or a fundamental, permanent shift in the distribution model.

Either way, the 2021 Model (as we’re calling it, temporarily at least) will have a huge impact on licensees in particular. Especially since it’s unclear whether the amount and cadence of promotional activity around streaming releases will match that which has traditionally accompanied theatrical debuts.

Caption: “Wonder Woman: 1984” was the first feature in Warner Bros’ slate to release simultaneously on streaming and in theaters on Christmas Day, setting the precedent for the studio’s 17 releases this year.

Is Black Friday dead?

Put more broadly, has the holiday retail calendar been permanently changed?

Last year, Amazon once again shifted the retail landscape, this time with its decision to push Prime Day to October, instead of the usual mid-July timeframe.

As dozens of other retailers jumped on the bandwagon to host their own competing sales, the result was an expanded holiday shopping window, kicking off more than a month before the traditional start – Black Friday.

That shift may not be unwelcome. “I think the majority of retailers would love to get out of Black Friday,” says Dean Allen, Chief Merchandising Officer at Mad Engine and a former Walmart buyer, noting both the sacrificed margins and a sales lull that inevitably followed the early burst of activity. “It’s something retailers started, but backed themselves into a hole they couldn’t get out of.”

All eyes are turned now to July, the traditional timeframe for Amazon’s Prime Day sales. The decision whether to return to regularly scheduled programming or maintain the new 2020 October timing could once again set the entire holiday calendar and answer Black Friday’s existential question once and for all.

Is there an impending experience explosion?

After nearly a year without sporting events, concerts, live shows, movie theaters and theme parks, consumers are chomping at the bit to get back out in the world. Whether and when they’ll feel safe enough to do so is another question.

After nearly a year without sporting events, concerts, live shows, movie theaters and theme parks, consumers are chomping at the bit to get back out in the world. Whether and when they’ll feel safe enough to do so is another question.

A good litmus test for the situation might be Disney. The company’s relative silence on theme parks in its recent investor day presentation, coupled with analyst forecasts that the live experiences side of the business won’t return to “full earning power” until Fiscal Year 2023, paints a dire picture.

Then again, another good litmus test for the situation might be history itself. the end of WWI and the Spanish flu pandemic ushered in the Roaring Twenties…

How important will the mask category continue to be?

When face masks burst on the scene last spring, it wasn’t clear whether they would be a short-term sales opportunity or a permanent part of fashion wardrobes.

Yet since July, with the promise of a vaccine on the horizon and consumers having already purchased baskets full of masks, sales have been declining.

Trevco, which was early in launching MaskClub.com, reported in November that they were seeing sales decline 10-15% from July levels, according to CEO Trevor George.

That’s not to say non-licensed and medical-grade face masks won’t continue to sell, but licensed versions, which carry a higher price, will likely decline more rapidly, predicts George.

Yet Concept One CEO Sam Hafif, remains optimistic about the mask category’s future despite also seeing a decline in sell-through.

“We do see masks as being a staple of people’s wardrobes along with socks and underwear, as Americans are now more aware of germ spread, and mask hygiene as a way to control the common cold and other viruses,” says Hafif.

Will cannabis reach a new high?

Cannabis brands appear ripe for licensing after several years of nibbling at the edges. As 2020 drew to a close there were growing signs cannabis was emerging as a consumer products category with licensing legs:

Cannabis brands appear ripe for licensing after several years of nibbling at the edges. As 2020 drew to a close there were growing signs cannabis was emerging as a consumer products category with licensing legs:

- Global cannabis industry sales were forecast to grow 38% last year to $19.7 billion, and increase 22% annually to $37 billion by 2023.

- Cannabis companies Aphria and Tilray agreed in December to a $4 billion merger, potentially creating the world’s largest cannabis company. Tilray brings with it a licensing agreement for Authentic Brands Group’s Nine West, Prince (the tennis brand) and other brands for CBD products.

- In November, Tilray CEO Brendan Kennedy said he thinks Europe is the next big growth opportunity for cannabis. “I think that we’ll see possibly the entire EU legalize cannabis for medical use over the course of the next, let’s call it, 18 months.”

- Across the pond, New Jersey, Arizona, South Dakota, and Montana legalized marijuana in November, further opening up the U.S. market to producers. Thirty-six U.S. states have now legalized marijuana for medical or recreational use, the latter being legal in 15 states.

- Additionally, the S. House passed a bill in December to decriminalize marijuana, although the legislation is likely to die in the Republican-controlled U.S. Senate.

- The arbiter of all things home, Martha Stewart, launched a line of CBD-based wellness products in September with Canopy Growth Corp. and followed it up with a CBD citrus-flavored wellness sampler two months later.

Obstacles do remain. For example, cannabis companies still can’t conduct business across state lines in the U.S., but cannabis industry executives are increasingly focusing on brand building.

“There are many brands that are strong in their own right with distinct value propositions” in non-cannabis categories, Canopy Growth CEO David Klein said in releasing third quarter financial results in November. “Building these brands today allows us to generate revenues without the headwinds of regulatory challenges. And then, we can extend these brands into CBD or even THC as regulations evolve.”

How will licensing agreements shift to account for all these business changes?

After a year like no other, with businesses shutting down, shipping delays and retail malaise, newly revised licensing contracts will come into play this year.

In 2020, some contracts were rewritten to reduce minimum guarantees and extend terms to allow licensees to recoup their losses. And while several licensors initially resisted changing contract terms at the start of the pandemic, those once iron-clad agreements proved malleable as companies were forced to adapt to the new normal.

Whether that spirit of cooperation and collegiality will continue, will be something to watch as the year advances.